![]()

![]()

PALMERSTON NORTH CITY COUNCIL

Committee of Council MEETING

10 June 2019

LATE ITEM

9. Finalising the Annual Budget (Plan) 2019/20 - Amendments Page 5

Memorandum, dated 5 June 2019 presented by the Strategy Manager Finance, Steve Paterson.

AGENDA

Committee of Council

Late Item

|

Grant Smith (Chairperson) |

|

|

Tangi Utikere (Deputy Chairperson) |

|

|

Brent Barrett |

Leonie Hapeta |

|

Susan Baty |

Jim Jefferies |

|

Rachel Bowen |

Lorna Johnson |

|

Adrian Broad |

Duncan McCann |

|

Gabrielle Bundy-Cooke |

Karen Naylor |

|

Vaughan Dennison |

Bruno Petrenas |

|

Lew Findlay QSM |

Aleisha Rutherford |

![]()

![]()

PALMERSTON NORTH CITY COUNCIL

Committee of Council MEETING

10 June 2019

LATE ITEM

9. Finalising the Annual Budget (Plan) 2019/20 - Amendments Page 5

Memorandum, dated 5 June 2019 presented by the Strategy Manager Finance, Steve Paterson.

![]()

![]()

PALMERSTON NORTH CITY COUNCIL

TO: Committee of Council

MEETING DATE: 10 June 2019

TITLE: Finalising the Annual Budget (Plan) 2019/20 - Amendments

DATE: 5 June 2019

Presented By: Steve Paterson, Strategy Manager Finance, Finance

APPROVED BY: Grant Elliott, Chief Financial Officer

1. ISSUE

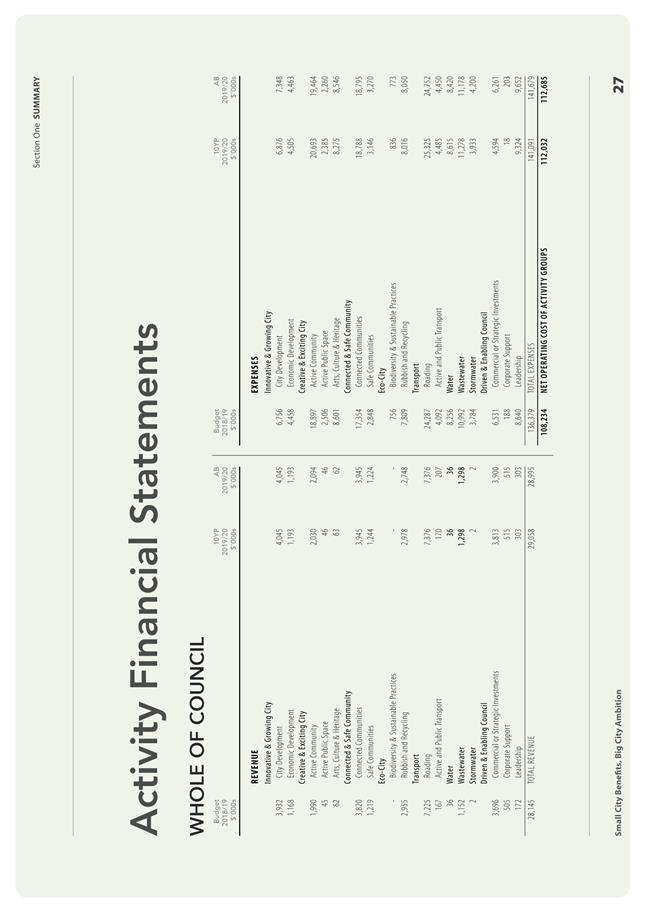

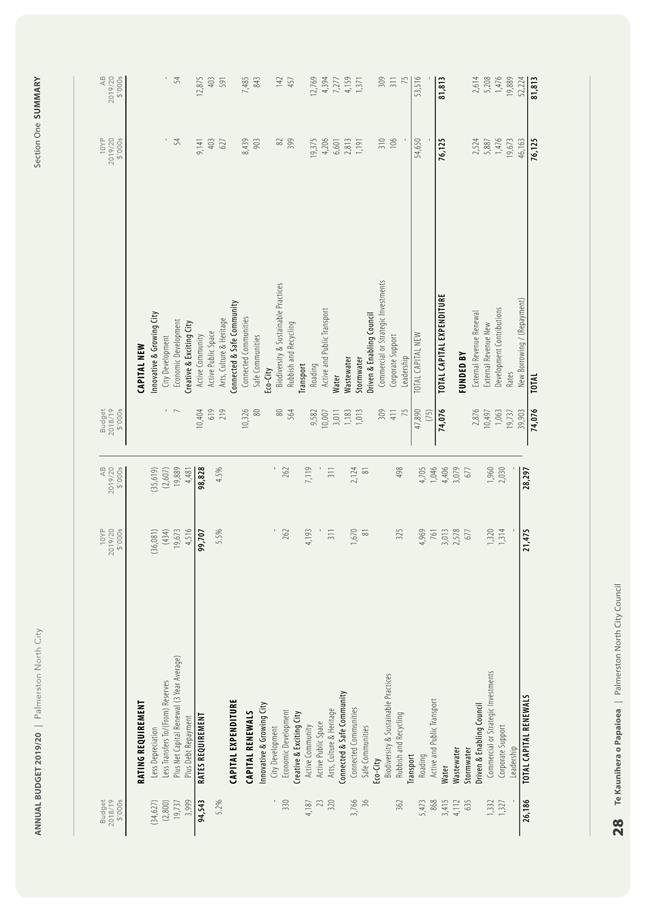

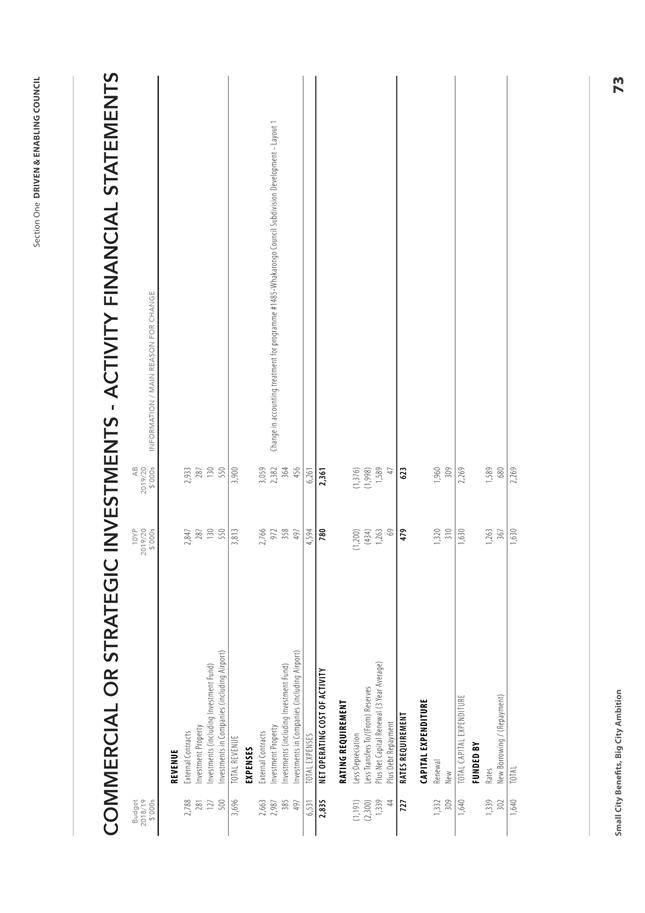

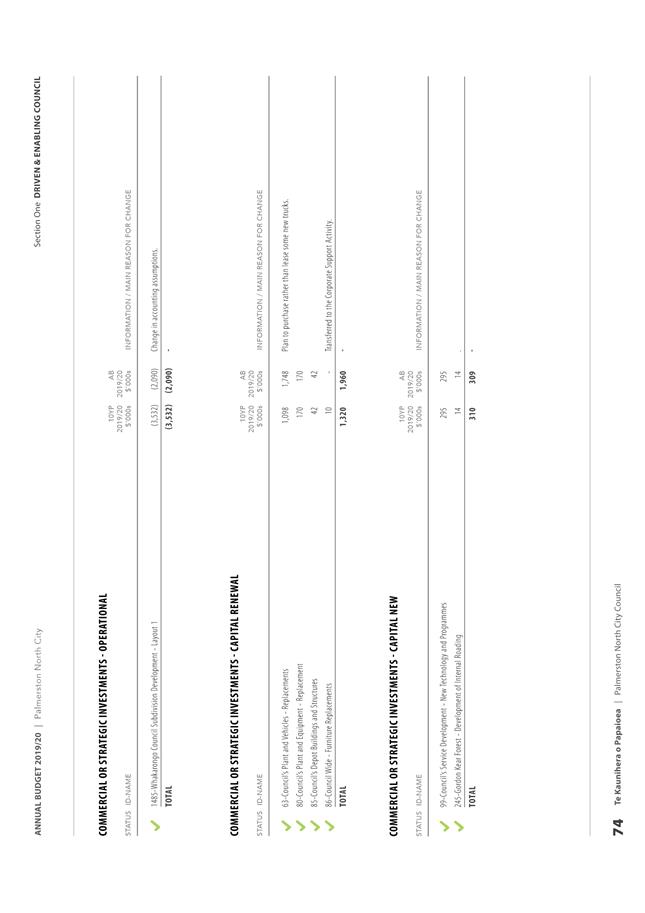

Item 7 on the Committee’s agenda relates to finalising the Annual Budget for 2019/20. It contains a memorandum dated 27 May 2019 and a draft of the Annual Budget document.

Since their preparation we have further reviewed the assumptions underlying them and now believe a change is required to them to reflect a more correct accounting treatment of the Council’s subdivision in Whakarongo.

2. BACKGROUND

At the Committee’s February meeting we explained that there had been a change to the way the Whakarongo subdivision was being accounted for by comparison with what had been done in the preparation of the 10 Year Plan.

As the subdivision is proposed to be actively developed and sold the land is now recorded as inventory and is revalued each year. The accounting treatment is that sales revenue will be recorded in the year of sale and the expenses will be those that relate to the specific sections that have been sold in that year.

In the 10 Year Plan it was assumed the total project would generate a cash surplus of approx. $10m (ie an operating surplus of approx. $6m over the present $4m value of the undeveloped land).

The present draft of the Annual Budget for 2019/20 assumes sales revenue of $4m for the year but also assumes $4m of costs to generate this revenue. On reflection this is an unrealistically conservative assumption. Based on the original assessment of the total costs for the project it would be more reasonable to allocate $2m of the costs to the 2019/20 year.

It is proposed this changed assumption be incorporated in the Annual Budget document and a series of consequential changes be made.

Attached are copies of the replacement pages of the document that will need to be changed.

These changes do not impact on the thrust of the budget, the level of rates required or the sums required to be borrowed.

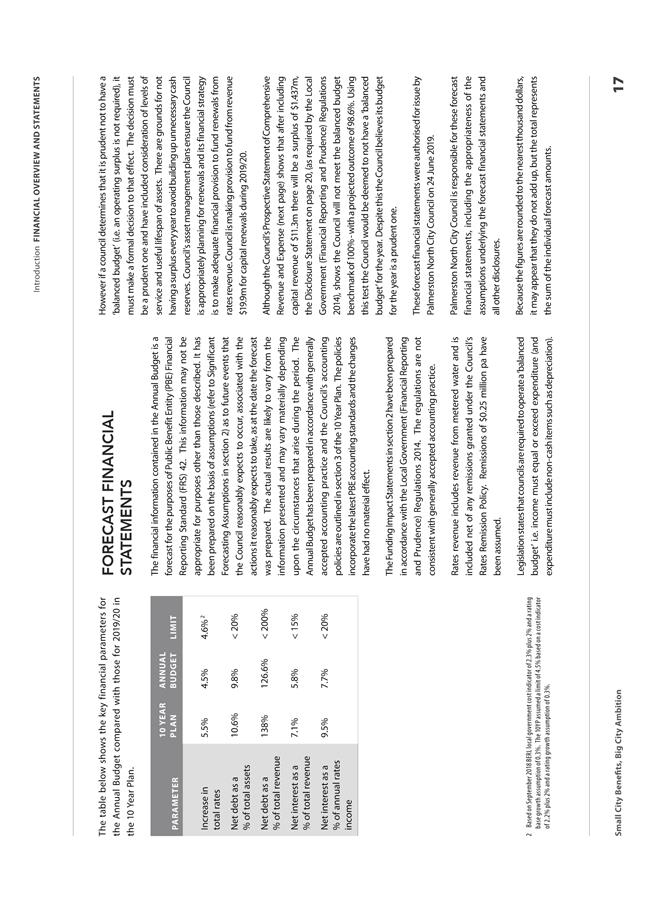

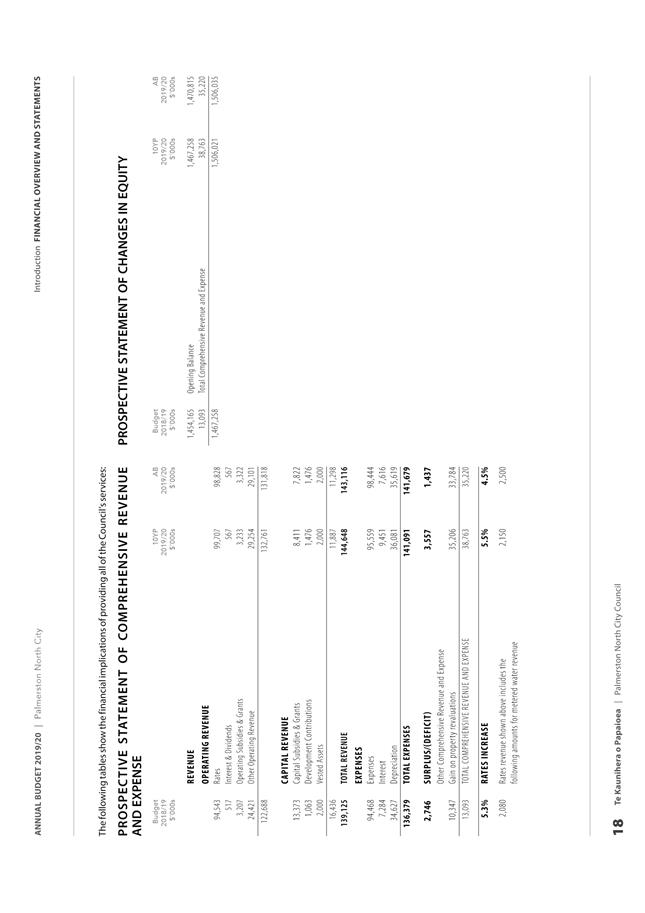

They do however impact of the test of whether or not the Council has a balanced budget – the matter that is addressed in section 3 of the memorandum of 27 May 2019. Rather than the $561k deficit referred to in that memorandum, the revised Prospective Statement of Comprehensive Statement of Revenue and Expense projects a surplus of $1.437m for the year.

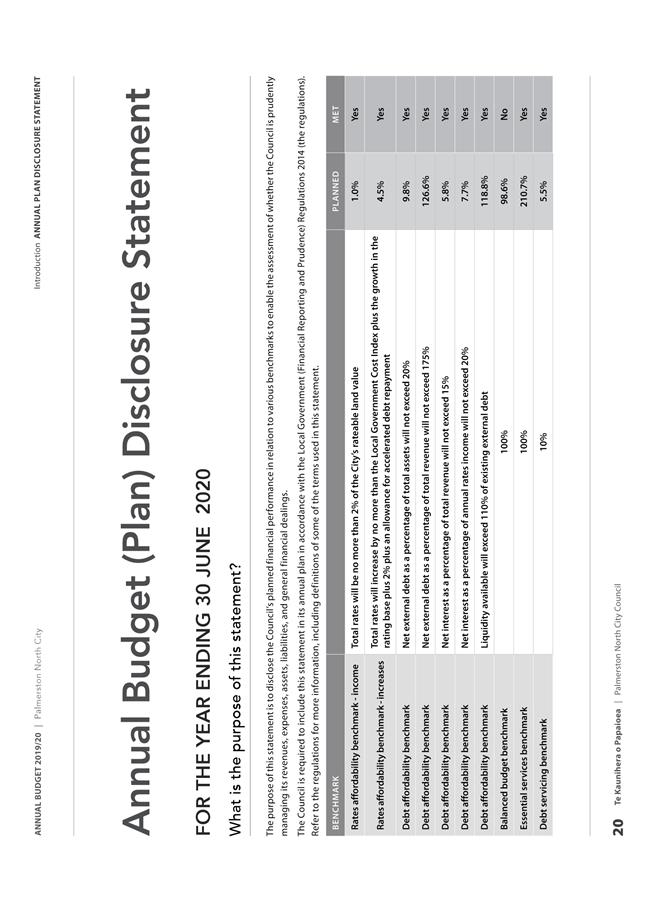

The methodology required by the Local Government (Financial Reporting and Prudence) Regulations 2014 for the Disclosure Statement (see pages 48-49 of the agenda) excludes development contributions and vested assets from being considered as part of revenue for the balanced budget test. With these items excluded the deficit for the year will be $2.04m (rather than the figure of $4.04m previously advised). This means the Disclosure Statement shows a planned outcome for the year of 98.6% against a benchmark of 100%.

For the reasons outlined in the 27 May memorandum the Council’s approach to funding the 2019/20 Annual budget is considered to be prudent. To be sure the Council has met the requirements of section 100 of the Local Government Act it is recommended a resolution be passed acknowledging there is a projected deficit using the calculation required by the regulations.

3. NEXT STEPS

Assuming the proposed changes are incorporated in the document the next steps will be as outlined in the memorandum of 27 May.

4. Compliance and administration

|

Does the Committee have delegated authority to decide?

|

No |

|

|

Are the decisions significant? |

No |

|

|

If they are significant do they affect land or a body of water? |

No |

|

|

Can this decision only be made through a 10 Year Plan? |

No |

|

|

Does this decision require consultation through the Special Consultative procedure? |

No |

|

|

Is there funding in the current Annual Plan for these actions? |

Yes |

|

|

Are the recommendations inconsistent with any of Council’s policies or plans? |

No |

|

|

The recommendations contribute to Goal 5: A Driven and Enabling Council |

||

|

The recommendations contribute to the outcomes of the Driven and Enabling Council Strategy |

||

|

The recommendations contribute to the achievement of action/actions in Not Applicable |

||

|

Contribution to strategic direction |

Refer to original memorandum dated 27 May 2019 |

|

|

1. |

Amended pages for Annual Budget document ⇩ |

|